Baidu Valuation Suggests a Reality Check but No Warnings

Baidu, Inc. (BIDU) has had - and continues to have - perhaps the best management of the global internet services companies. That’s quite a put down for the big guys in the U.S. Baidu is a clearly stabilizing and fast growing organization. The company has only been growing since 2006 and is making great headway. However, in my work it does not qualify as a “quality” firm – yet! Keep in mind that there are other, often smaller, internet firms that are more conservative, but few have produced any better investor ROI over recent years.

Earning estimates on balance are definitely positive for the near-term, and should continue improving for a long time. How the Street will reward or punish Baidu, or any other company in the future, is always questionable. It appears, according to comparative analytics, that the upside is becoming quite limited and that the downside currently has more appeal. With momentum and relative strength at current levels, shorting is out of the question, but hedging or taking profits may be a prudent strategy.

My analytics, to a large degree, have to do with comparative analytics. Comparing Baidu with its peers - and other top capitalization/revenue producing companies in general - provides a clear and very positive story of both the company and the internet services industry group.

Timely news includes the fact that higher projected earnings growth in the near-term have been much better than expected.

As a sector, the technology – internet arena and its component companies, particularly those similar to Baidu, have been difficult for investors to profit from. This is likely due to the revenue-dynamics that evaluations are often tough to figure. Firms like Baidu are clearly in focus within a negative economy and are perhaps best left for traders - and not long-term investors - to consider.

My analytic focus (to invest or not to invest) on any company is most heavily weighted on fundamentals. Baidu appears to have the prospect of improving earnings in the longer- term, but I still feel it is a “trading stock” and not yet an investment grade company. For me, this is just a warning (something to consider) prior to buying. For prudent investing, those earnings will have to remain strong over a quarter or two (or more) before I would consider it a “wise investment”.

Fundamental Valuation Analytics Table

(Weighting 40%)

Baidu, Inc. (BIDU) Compared to Apple, Inc. (AAPL)

Stock and Symbol | Approx. Current Price | My Target Price % Above (+) / Below (-) Current Price – Valuation is “Tweaked.” One Year Projections from the next - - Bullish Inflection Point. | PEG | P/E | Forward P/E | Valuation Divergence (%) (One - Year Projected to a Mean) from the next - - Bullish Inflection Point. |

Baidu, Inc. (BIDU) | 118 | + 5 to + 12+% | 0.85 Very Good | 76.5 | 33.4 | 126% |

Comments: Obviously this is an exceptionally “excellent” valuation and target price projection. This is why it is wise to compare - and frequently. Care is signaled by the P/E multiples but for a trader – who cares? This work / analytics is for you to possibly take positions at a future date, but definitely not at this time. | ||||||

Apple, Inc. (AAPL) | 345 | + 20 to + 40+% | 0.72 | 18.9 | 13.0 | 45% |

Comments: Obviously this is a very good to “excellent” valuation and target price projection. When you do further fundamental analysis, it looks even better. Add to that the technical and consensus analysis and you have confirmation that AAPL is and remains a winner. This is why it is wise to compare - and frequently. My work / analytics is for you to possibly take positions at a future date, but definitely not at this time. | ||||||

Additional Related Comments

I always compare Apple, Inc. (AAPL) with my other “bellwether” companies, as well as those I am considering for investment. (For me, Apple is numero uno!) I then do a quantitative rating for my weighted fundamental, technical, and consensus analysis. Currently this is my summary ranking.

- BIDU: Rating: Fundamental: Excellent; Technical: Excellent; Consensus: Very Good.

- AAPL: Rating: Fundamental: Excellent; Technical: Very Good; Consensus: Excellent.

Notes for the above table and for your information:

- Fundamental valuation - Data in today’s marketplace requires me to look carefully at the numbers as being either realistic or creative. That’s because more recently, financial analysts are using new/funny math and have changed the criterion on basic valuation. This is producing many valuation data inconsistencies, so I have adopted an additional procedure that I call “tweaking the results." This procedure is sometimes needed to get me back to ‘realistic’ valuations. It requires having an eye on the short and intermediate-term company price movement, but is definitely not a part of my technical analysis. My valuations also consider the two-year - forward P/E data, but is not weighted heavily. Using this procedure produces very accurate analytics for decisions at bullish and bearish inflection points.

- Most financial analysts determine the price target range by estimating a future earnings per share and then applying a price-to-earnings multiple, also known as the price earnings ratio. I prefer to calculate price targets (high / low) for both the current and next fiscal year by applying the stock's present multiple to the average analyst's estimates and follow with some foxy "tweaking" of the results.

- Further, I believe that there should be just two aspects of fundamental valuation. They are the now and the later, which translates to 1-2 years and more than three years but not 10 years. Obviously, the farther out we try to project earnings and cash flow, the more inaccurate the data becomes. That is why I do my valuations rather frequently, especially around times of anticipating inflection points.

- PEGs: You will note that some of these companies are carrying high or sometimes negative PEG ratios. I consider the PEGs very important when deciding to take positions in a given security.

Since coming out of retirement in October 2007, I have witnessed a vast change in the valuation practices being offered by many financial analysts. The shenanigans and other accounting practice games were active before, but have now reached a new height of deception. The general public is often lazy about learning, and perhaps naive. The financial analysts know that these characteristics exist and now are taking advantage. It's simple: The average Investor is asking to be told that all is "ok,” so that is what they are being told.

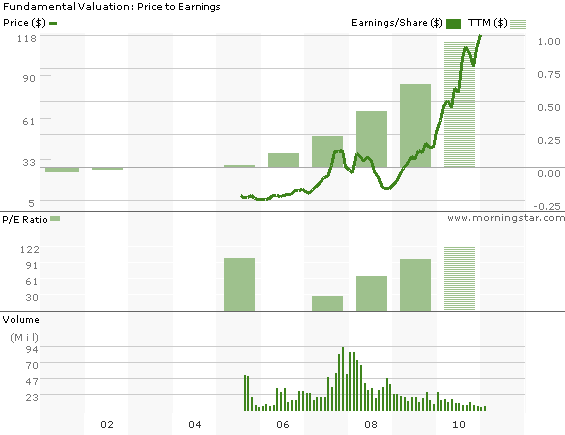

The graphic below (click to enlarge) tells the earnings story very well and should be studied with a discerning mindset.

Morningstar earnings chart:

As for the financial statements, all look (“look” can be a deceiving word) very good. However, nothing appears positive or compelling. In summary, the operating income, net income and balance sheet all increased/improved, and appear to be on track.

Technical Thoughts/Analytics

(Weighting 35%)

The price activity for Baidu continued to improve since the February 2009 lows at an awesome pace. These numbers (prices) are an important consideration before making an investment decision to buy or short any security.

Baudu, Inc. price targets are more than compelling.

My current marketplace position is: I am waiting for this current rally to run its course and am focused on identification of the next bearish inflection point. For BIDU it is pretty much the same story.

Notes for My Technical Work

a) Investing Wisely: This means taking long positions in companies and ETFs at or around Bullish Inflection Points. And just the opposite at Bearish Inflection Points.

b) Trading Wisely: This means taking long positions in high momentum / relative Strength companies and ETFs during Bullish time frames – on dips. And just the opposite during Bearish time frames.

Consensus Thoughts/Analytics

(Weighting 25%)

Consensus analysis for me is very important. Please note the high percentage weighting I use. There is an old saying: If the Street does not like the company, don’t buy it.

My rankings for Baidu is “very, very good.”

So for this old bearish fox, I’m very pleased with the fundamental statistics/indicators, love my technical charts and my consensus work is simply right on.

Economic Note: Economically speaking there is always a concern or question as to what the U. S. Federal Reserve Board may or may not do regarding the management of the economy. We do know that rallies have come when the Fed injects capital or fiscal stimulus into the economic system, but that is becoming an "old news" factor. How this plays out over the coming few years, for me, is quite problematic.

Conclusion

My focus is “investing wisely”, e.g. taking advantage of the bull / bear cycles as they occur within the overall marketplace. Integrating modern fundamental analytics within these technical cycles means maintaining a process of the thorough and ongoing analysis of many companies and industry groups in my universe. This is a vital discipline in “investing wisely.”

While I believe the general market is in for a meaningful pullback, the prevailing question from most investors is: When? How big and how long will it be? Do I hold my current positions or do I sell? Is there a profitable alternative? The answer will be obviously quite clear when the pullback is over but an old axiom for profitable investing tells us to be prudent in times like this. You might want to remember that cash is always an excellent safe harbor. However, if you are a proactive investor, taking bearish positions may also be wise.

As I mentioned, when “investing wisely,” we must take advantage of the bull/bear cycles as they occur within the overall marketplace. These cycles are both economic and stock market related in nature and must be carefully and frequently analyzed. Within the stock market, you can integrate modern analytics within these “cycles.” This also means that I maintain a comprehensive process of the thorough economic, fundamental, technical and consensus analysis of many companies, 15 sectors and more than 200 industry groups in my universe. I believe that this discipline provides the necessary clarity regarding the rotation that the economy and almost all sectors, industry groups and companies go through – from favorable times to unfavorable times and perhaps back again. Few investors seem to understand that it the same for the economy. The world continues to produce an economic “cycle” effect that continues as a process - like life itself.

My economic work is just another one of many “bellwether” forms of research/analytics to help identify prudent securities for buying and for short selling as the marketplace cycles from bull to bear and back again - over, and over and over again.

The good news about the marketplace is that we are presented frequent and conservative/low risk opportunities to invest long, invest short or to simply to hold cash. For me, this is called “investing wisely.”

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Comments